Swimming with the Tide: How IIFL Capital Is Transforming from Brokerage to a Full‑Service Capital Markets Powerhouse

In India’s ever-evolving capital markets, few firms have managed to transform as effectively as IIFL Capital Services Ltd. What started as a traditional brokerage is now well on its way to becoming a full-service, technology-enabled capital markets powerhouse. But is it a stock worth owning? Let’s dive deep.

“Only when the tide goes out do you discover who’s been swimming naked.”

— Warren Buffett

🌐 Industry Backdrop: Storms and Survivors

India’s broking industry is in flux. Over the past year:

SEBI’s regulatory tightening on index derivatives severely impacted volume-driven brokers—daily turnover dropped 30–70% in segments like Bank Nifty options.

Retail investor participation remains robust but is shifting toward long-term SIPs and wealth advisory.

Amid this, only players with diversified offerings, deep research capabilities, and strong digital platforms are likely to thrive.

🏆 Why IIFL Capital Stands Out

1. Strategic Business Evolution

From a traditional broker, IIFL now spans:

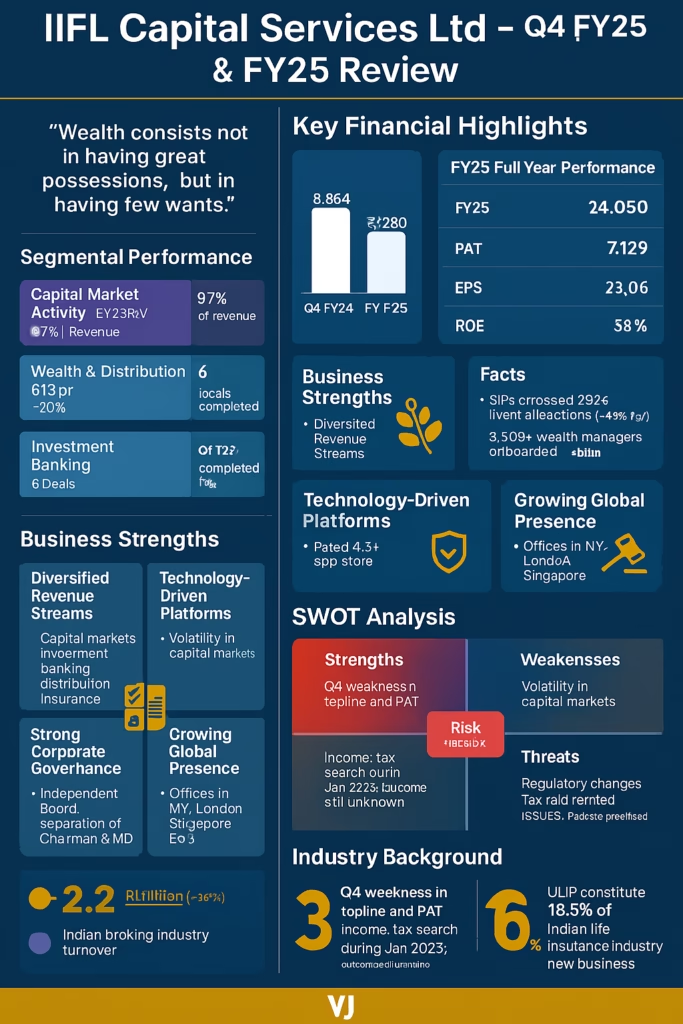

Institutional Equities & Research: 299 stocks under coverage, 44 analysts—one of India’s most extensive networks.

Investment Banking: Completed 6 deals in Q4FY25, including the ₹87,500 mn Hexaware IPO. Pipeline of DRHPs and mandates looks robust for FY26.

Wealth Management: ₹313 bn in distribution AUM (+20% YoY), 3,500+ wealth managers, and rising SIP penetration.

Insurance, PMS & AIFs: Key product expansions to diversify beyond cyclic equity markets.

2. Solid Financial Footing

FY25 PAT: ₹7,129 mn (+39% YoY)

ROE: 33%

EPS CAGR (5Y): ~34%

Net Worth: ₹25.1 bn

3. Strong Governance & ESG

Independent Board (50%)

Separate Chairman & MD roles

LEED-certified offices, solar initiatives, digital onboarding (99% paperless)

“Know what you own, and know why you own it.”

— Peter Lynch

🚀 What Could Drive Future Growth?

| 🚀 Growth Engine | 🔑 Catalyst |

|---|---|

| Investment Banking | Strong IPO/QIP pipeline, mandates from growth sectors |

| Wealth Management | Rising SIP flows, HNI/UHNI platform, fee-based income |

| Product Diversification | Pre-IPO deals, real estate funds, insurance broking |

| Digital Adoption | AI-driven advisory, wealth manager portals, scalable partner integrations |

| Geographic Expansion | Teams in NY, London, Singapore for cross-border origination |

🧱 Risk Matrix

| Risk Type | Description | Likelihood | Impact | Mitigation |

|---|---|---|---|---|

| Regulatory Risk | Derivatives regulation (e.g. SEBI rules on Nifty contracts) | High | High | Diversification into IB, Wealth, AIFs |

| Market Risk | Equity market correction impacting volumes & sentiment | Medium | High | Recurring revenue from SIPs, Insurance |

| Execution Risk | Scaling investment banking and HNI services effectively | Medium | Medium | Senior hires, cross-selling via tech |

| Competition Risk | Pressure from discount brokers (Zerodha, Angel One) and fintech platforms | High | Medium | Focus on full-service, advisory-rich model |

| Reputation/Tax Risk | Ongoing income tax investigation from Jan 2025 search (no outcome yet) | Low | Medium | Strong disclosure and governance measures |

📝 SWOT Summary

| Strengths | Weaknesses |

|---|---|

| • Diversified offerings beyond broking | • Q4FY25 revenues declined 22% YoY |

| • High ROE and strong balance sheet | • Still exposed to market cyclicality |

| • Trusted brand and global footprint | • Dependency on capital markets |

| Opportunities | Threats |

|---|---|

| • Rising wealth AUM & SIP growth | • Regulatory tightening and tech disruptions |

| • Growth in alternative products (AIF, PMS, pre-IPO) | • Margin compression in core broking |

| • Cross-border capital raising | • Global macro headwinds |

🤝 The Investor’s Question: Should You Buy?

IIFL isn’t just riding the wave—it’s building a vessel that can sail through storms. With a long runway in investment banking, wealth management, and alternative products, it has positioned itself well for India’s financialization trend.

But like any capital-market player, it is not immune to cycles. The derivatives regulation hurt Q4, and it will need to prove its mettle in growing recurring fee income.

If you’re an investor who believes in owning businesses that evolve with the economy, compound earnings, and generate return on capital, IIFL Capital deserves a place on your watchlist—if not in your portfolio.

“The stock market is filled with individuals who know the price of everything but the value of nothing.”

— Philip Fisher

💬 Over to You:

Would you rather own a pure-play discount broker, or a diversified capital-markets platform like IIFL?

Do you think India’s next bull market will be led by firms that offer more than just low-cost execution?

📩 Drop your thoughts below. Want a valuation model or competitor comparison next? Let me know!

Disclaimer:

This blog post is for informational purposes only and should not be construed as financial advice. The views and opinions expressed in this blog post are solely those of the author and do not necessarily reflect the views or opinions of any other individual or entity.

The author is not a SEBI-registered investment advisor. The information provided in this blog post is based on the author’s research and analysis and may not be accurate or complete.

The author may hold a position in the securities mentioned in this blog post and may increase or decrease their position at any time.

Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions.

Past performance is not indicative of future results.

Investing in securities involves significant risks, including the risk of loss of principal.