Zomato: Redefining Convenience and Competition in Food Delivery

What comes to mind when you think about food delivery in India? Chances are, Zomato is at the top of the list. Synonymous with innovation and reliability, Zomato has revolutionized the way Indians dine. Recently, the company hit a market capitalization of INR 294,000 crore, surpassing giants like Bajaj Auto, D’Mart, and Nestlé. But is Zomato’s meteoric rise sustainable? Can its market valuation withstand scrutiny? Let’s dive deep into Zomato’s journey, its potential, and the critical question: Is Zomato truly worth the hype?

What Makes Zomato Tick?

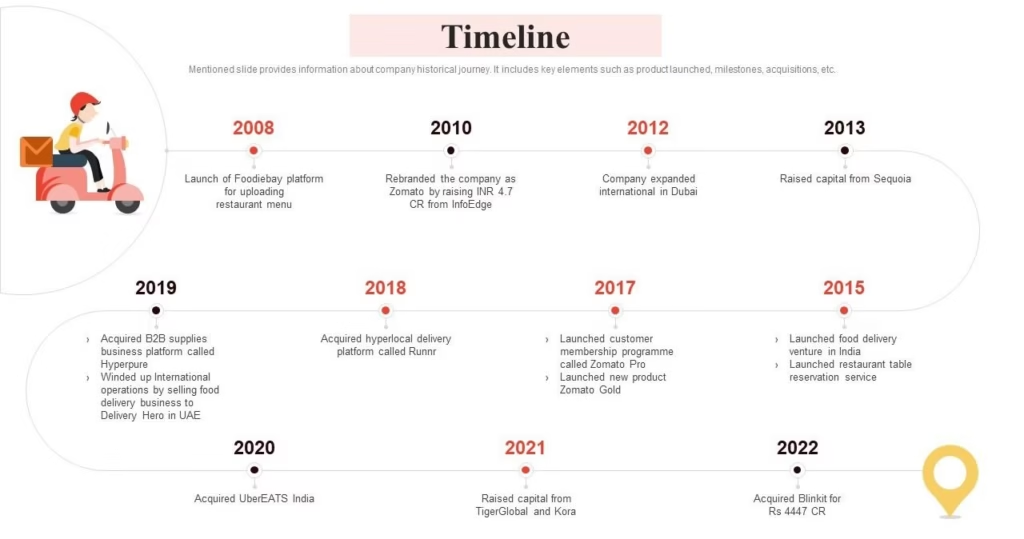

Zomato began its journey in 2008 as “Foodiebay,” primarily offering restaurant menus and information. An interesting tidbit from its early days: the founders initially hand-collected menu cards from restaurants around Delhi to upload on the platform—a humble beginning that laid the groundwork for a food-tech revolution. Fast forward to today, it’s a comprehensive platform that delivers much more than food. Here’s how Zomato has transformed the food and dining experience:

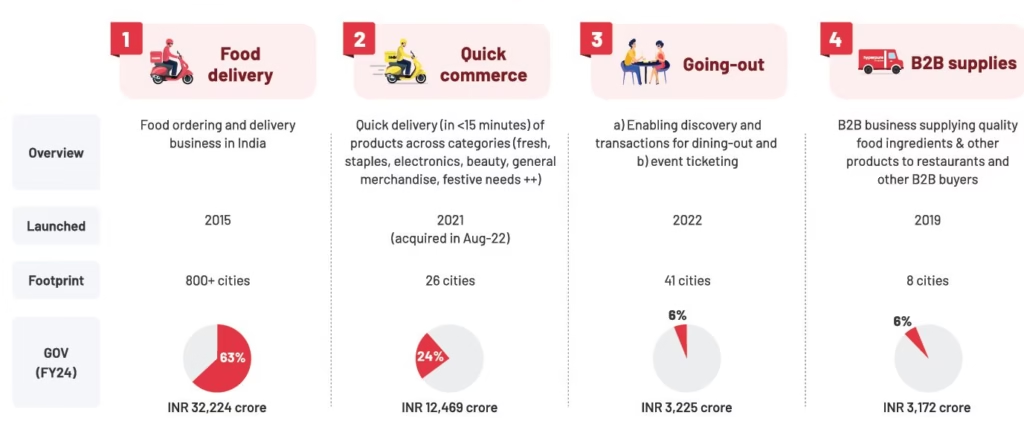

- Restaurant Discovery: A seamless interface to explore menus, reviews, and ratings.

- Online Ordering & Delivery: A robust network connecting customers and restaurants.

- Table Reservations: Simplifying dining out with hassle-free bookings.

- Zomato Pro: Exclusive benefits for members, including discounts and priority service.

This evolution isn’t just about adding features; it’s about strategically catering to three pivotal stakeholders:

- Riders: Competitive pay, flexible hours, and insurance benefits create a motivated workforce.

- Customers: Convenience, speed, and a diverse selection keep users coming back.

- Restaurants: Marketing tools, data insights, and enhanced visibility help partners grow.

A Booming Market: What Lies Ahead?

The Indian food delivery industry is on fire, with market projections showcasing a jaw-dropping leap from $36.3 billion today to $257.7 billion by 2032—a true testament to its meteoric rise and untapped potential. A report by IMARC Group predicts that the market, currently valued at $36.3 billion, will grow at a staggering CAGR of 34.32% to reach $257.7 billion by 2032. Similarly, the quick commerce sector is projected to triple in size, from $3.34 billion in 2024 to $9.95 billion by 2029.

But is this growth sustainable? Here are the key drivers:

- Rising Disposable Income: More spending power means higher demand for convenience.

- Urbanization: Busy lifestyles in growing cities create a fertile ground for delivery services.

- Tech Advancements: Faster deliveries and user-friendly platforms enhance customer satisfaction.

The Competitive Landscape: Zomato vs. Swiggy

Zomato surges ahead with a commanding 57% market share in the Indian food delivery sector, leaving Swiggy trailing at 43%. Zomato’s year-on-year Gross Order Value (GOV) growth stands at 31%, outpacing Swiggy’s 26%.

But does this make Zomato a foolproof investment? The adage “Even the best businesses can be overpriced” reminds us to tread carefully.

Forecasting Zomato’s Future

To evaluate Zomato’s potential, let’s break down some numbers:

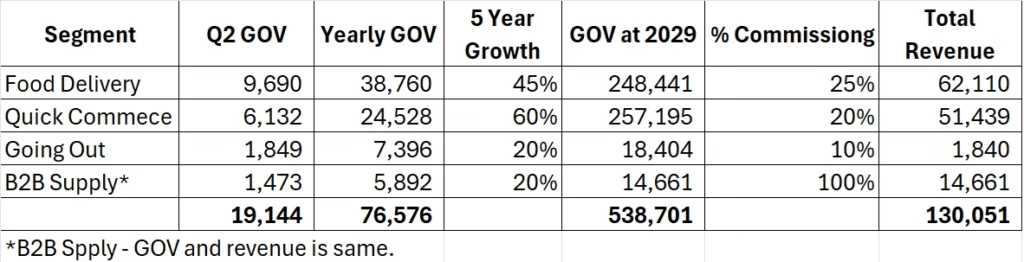

- Current GOV: INR 17,671 crore (Q2) + INR 1,472 crore (B2B revenue).

- Projected GOV for 2029: INR 538,701 crore.

- Revenue (2029): With a consistent commission rate, this equates to INR 130,051 crore.

Now, profitability becomes the big question. Mature players like Meituan (China) and Uber Eats (USA) operate with profit margins of 5% and 3%, respectively. If Zomato maintains or improves its operational efficiency, it could achieve margins of 5-10%, resulting in a profit after tax of INR 6,500-13,500 crore by 2029.

The Valuation Puzzle

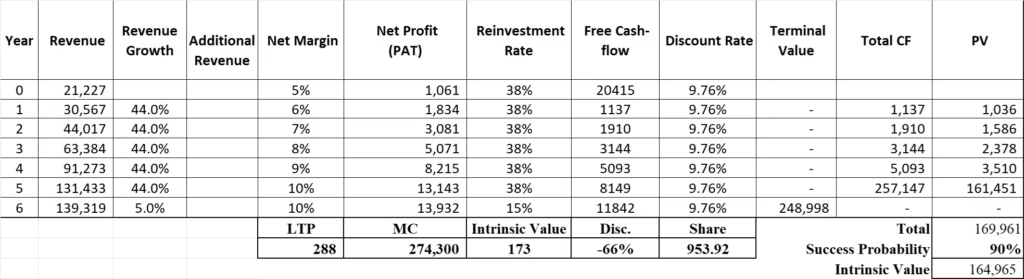

Using discounted cash-flow analysis, Zomato’s intrinsic value is estimated at INR 173 per share. This assumes:

- 44% growth without heavy reinvestment.

- Improved margins (up to 10%) by 2029.

- ROE aligning with technology companies.

Optimists may argue that the growth trajectory should be extended to ten years or that a 15% margin should be projected, resulting in INR 813,800 Cr in revenue and INR 122,000 cr in net profit by the end of 2034. But is it realistic to envision such dominance without intensified competition? After all, Amazon is one of the rare companies that managed such an extended period of high revenue growth—but examples like this are few and far between.

The debate is far from over. Is Zomato’s valuation a bubble waiting to burst, or is it just the beginning of a larger success story? Do you see Zomato maintaining its growth momentum, or will competition tip the scales? How do you see competition shaping the landscape? What’s your take on its current valuation—undervalued, fair, or inflated?

We will only know the correct answer in due time, but everyone has their own personal opinions.

Each individual can modify the numbers based on how they view Zomato in order to assess the service’s value and the price they are prepared to pay. Share your value for Zomat and any areas or presumptions you disagree with. Every reader will get a second opinion from this.

Disclaimer:

This blog post is for informational purposes only and should not be construed as financial advice. The views and opinions expressed in this blog post are solely those of the author and do not necessarily reflect the views or opinions of any other individual or entity.

The author is not a SEBI-registered investment advisor. The information provided in this blog post is based on the author’s research and analysis and may not be accurate or complete.

The author may hold a position in the securities mentioned in this blog post and may increase or decrease their position at any time.

Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions.

Past performance is not indicative of future results.

Investing in securities involves significant risks, including the risk of loss of principal.